Yes there is also a retail or end user one which is the one which we use

Guys, I need help with this.

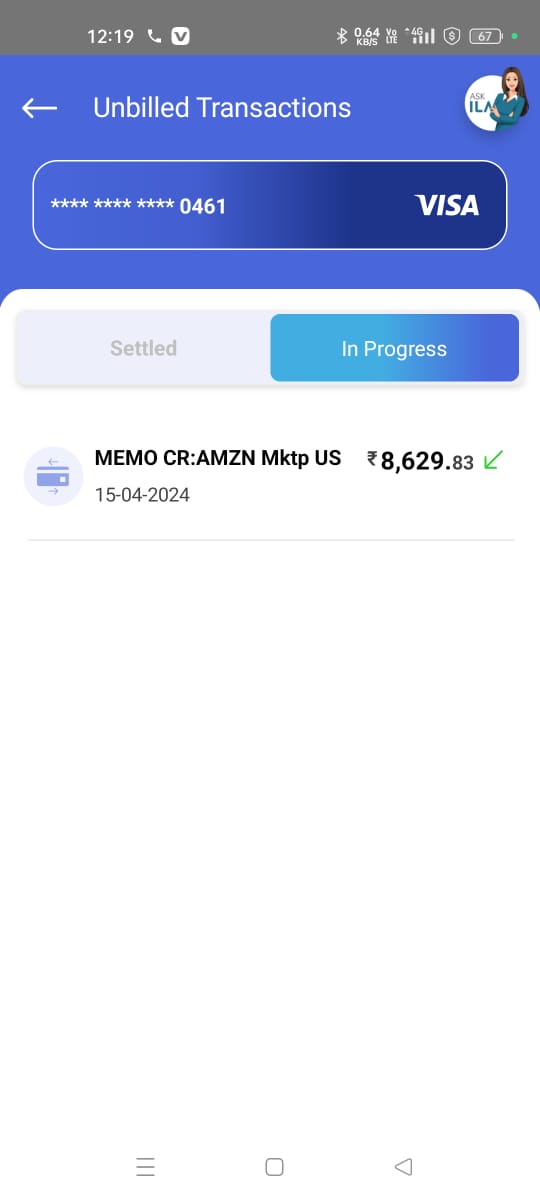

In March, I made a payment with my SBI card to Amazon.com (an international payment of ₹8,629), but the payment was canceled for no reason. Later, I tried with my RBL card, and it went through.

Amazon refunded me the amount, and it was visible in the unbilled section of the MySBI app for one day, but then it disappeared. It’s been 3 months, but the amount is still deducted, and I have not received it back on my card. SBI says no payment was reversed.

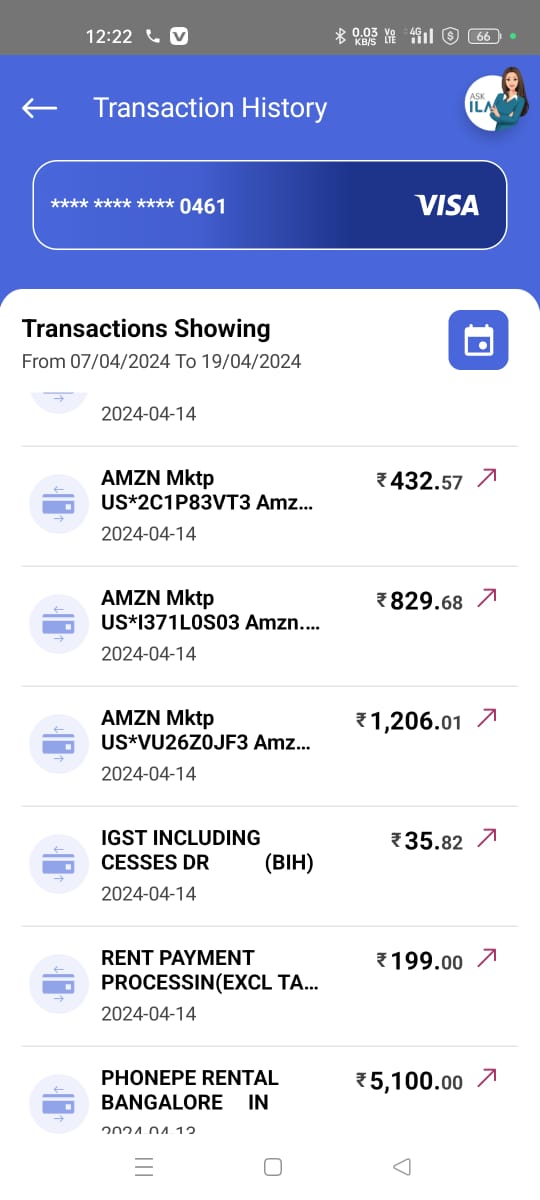

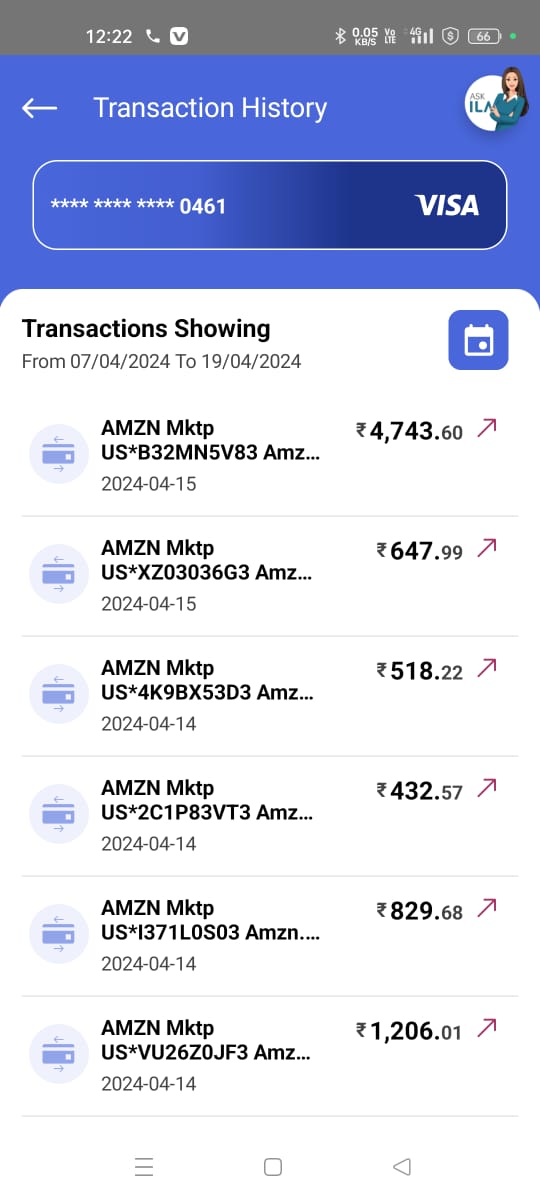

See the attached photo; it shows the payment in the MySBI app, but it disappeared after a day. In another photo, you can see the amount was deducted in parts (9 times, to be exact), totaling ₹8,629.

@@nRiTeCh @@honest1

I’m currently in a trouble as my credit card due date is 3’rd August but my salary hasn’t been credited yet. My salary was issued through a DCCB but the NEFT is pending because of the “C-Edge Technologies” issue. The remitter bank hasn’t received the amount back and as per the bank manager’s words, it will be credited latest by 3’rd Aug. If for some reason, it gets delayed by another day, what should I do?

I’ve already cleared appx 30% of statement balance already by my savings balance, so minimum amount is already paid. How do I claim the 3 days extra peroid by RBI ?

There is generally a buffer of 2-3 days which banks allows for CC payment. (As earlier cheque were used to make the payment and its realisation used to take 2-3 days)

Why was the amount deducted in part? Did you made 9 different purchases separately?

You should be contacting amazon.com support in the regards as if they have done a reversal for the refund. Once thats clarified you can get hold of sbi.

You might have also received a refund from amazon which you can forward to sbi as an evidence and slo the order history snapshot where it says refunded for cancellation or payment failed etc. reasons.

Credit score impact happens when you don’t pay your Minimum Amount Due

Secondly let’s say you have paid 1-3 days after your due date then you can call CC or mail cc to request relaxation of interest on the remaining amount payable

Use cred (hot take) payment gets realised instantly

Make a dummy transaction by entering wrong otp or cvv. Then call the helpdesk of your bank and ask for MCC of the merchant. This is the fastest way to know.

Yes, MCC codes are same for all banks. They are dependent on merchant and not the bank. Banks usually allow rewards on certain mcc codes, these vary from bank to bank and card to card.

1 Like

no it was a single order id only they deduct sometimes in parts. amazon has not sent any mail in this regard currently and on asking they simply state to contact your credit card co.

its just like amazon.in if your payment fails for some reason , their is a notification in order to retry payment so I retried with other card and it was a success.

You should check all transaction from 15th to today. If the amount isn’t there then call 1860 500 1290. On call menu click 1 > click again 1> enter your yr of birth> then click 2> click1 > click 9 if still agent not available, then > click1

You will get connected to CS, they will help in this issue. Surprisingly, SBI CS is very helpful and prompt.

Generally banks allow a grace period of 2-3 days for settling bill after due date. Use Cred for instant bill settlement or directly the banks portal.

Should one get a CC if he/she rarely orders things and/or their online purchases are extremely minimal?

Yes cuz credit score

1 Like

Check you bank statement if the reversal or deductions shows up. You can then chat with amazon.

Just FYI for everyone..SBI or any public bank cars suck for international transactions so better to go the private way and before even thinking of doing international payments ensure the options are enabled for your card/account as these days those options come disabled by-default!

Well IDFC app shows MCC code for transaction that’s what i’ve been told by my friend who works in the Data Science team there

Speaking from own experience or guess? If own experience then getting 800+ cibil score or keeping it for more than a few weeks requires a very high quality secured loan which typically means either home loan or education loan for studying in some tier 1 institute here or abroad. Also, despite doing all this there is no guarantee of 800+ cibil score.

@@honest1 There is no suhc thing as “dodging the algo”.

Just to make sure check your amazon.com acc to see they haven’t added the amt as amazon wallet balance.

As per RBI rules if due date is 3rd & you pay within next 3 days (pay here does not only mean you paying but also bank receiving it as depending on factors the payment may be delayed by a day if using 3rd party apps/websites) then paying by the end of 6th should be fine. Use credit card bank’s own payment gateway/pay bill option.

This does not work for all banks, most likely only works with HDFC & few other banks.

Theoretically true but not practically. Banks may assign/interpret their own “definition” of MCC code to payment gateways as per their discretion which is why you see same gateway being tagged as “utility” by some banks while “rent” as some other banks (because their cards still giving rewards on rent txns).

You must be one of the luckiest members ever to join TE because as per majority (incl own experience multiple times) SBI card CC is one of the worst among all credit card providers (worst I would say is BoB which actually charged a late payment fee & interest charge for a 50 paisa (yes that’s paisa) total due amt which user forgot to pay by due date).

No unless one can be sure not to fall into the trap of overspending/reward hunting. In any case it is not recommended for those still in college studying.

Is there any real benefit to an 800+ cibil? As long as your cibil is >750, I haven’t seen it make an impact on credit card approvals, limits etc.

Out of curiosity:

There are multiple Credit Bureaus in India. Which one do banks normally prefer when issuing a CC?

For example, the following are my scores (as of July '24):

CIBIL: 740

Highmark: 861

Equifax: 747

Experian (lowest): 640

Almost every bank uses CIBIL, while experian being used rarely.

1 Like

Someone told me to pay my credit card bill using “cred” to get 1-2 % cashback.

Is there any risk in doing so?

Any other alternatives

I’ve been using Cred for the last 5 years for paying my CC bills.

The cashback you get is random (and usually meh). For example, once I just got 1 re (not a typo) of cashback for paying a CC bill of 50k. In another instance, I got 15 rs for paying a CC bill of 2k.

Cred payments are usually very fast, and risk-free. There are other perks such as shopping discounts using coins that you earn after every CC payment. A lot of other features are present that may or may not be useful to you, such as Cred Garage, for tracking vehicle-based spends (which I find useful).

1 Like

There is no app/website which gives 2% cashback, heck even 1% uncapped.

The best way to get 1% cashback is using HDFC Billpay portal with HDFC Platinum Debit Card to pay Credit card bills of banks other than HDFC itself. This way you’ll get at max 750rs cashback in a calendar month.

2 Likes