raksrules

Oracle

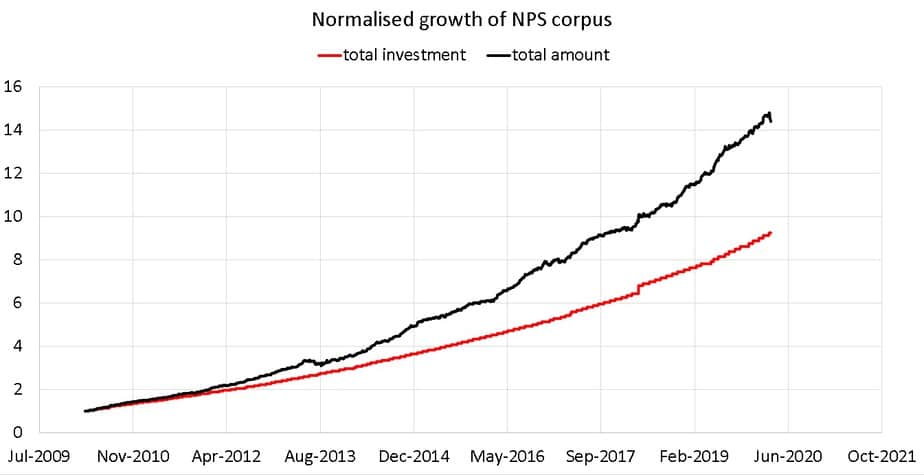

Recently In my organization, they conducted a web meet to explain about National Pension Scheme (NPS). They explained about Tier 1 and Tier 2 and where tax benefit is there. In first instance, the savings look great with the compounded interest and per month contribution doesn't look big too. All appears great and worth going on.

But then I further googled and also checked /r/Indiainvestment on reddit and seems NPS is not as good as it seems for few of the reasons like...

So anyone here who is currently putting money in NPS. What prompted you to do this? Do you see any benefit as you see it as guaranteed return versus mutual funds and such?

Any other comments you may have related to NPS for or against the scheme.

But then I further googled and also checked /r/Indiainvestment on reddit and seems NPS is not as good as it seems for few of the reasons like...

- Only 60% corpus can be taken and that too only when one retires (Age 60 approx). Rest 40% goes into Annuity which is mandatory.

- Even under new regime, Tax benefits beyond 80C can be availed. But there is no guarantee that the tax benefit may be there in future.

- There is no way to just exit the scheme anytime and best option is to take 20% out before one retires. Basically, money is locked.

- The companies which manage the NPS are all private.

So anyone here who is currently putting money in NPS. What prompted you to do this? Do you see any benefit as you see it as guaranteed return versus mutual funds and such?

Any other comments you may have related to NPS for or against the scheme.