veera_champ

Forerunner

Happy to help mateThx to @veera_champ, for helping me get a good deal on 5600

Happy to help mateThx to @veera_champ, for helping me get a good deal on 5600

Welcome.Thanks a lot @solo_wing for helping me save 1k+!

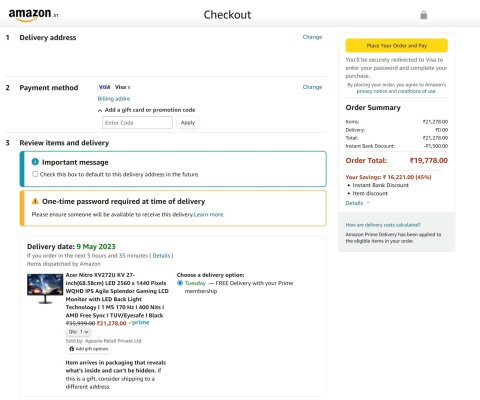

Can anyone with Amazon Pay ICICI Bank CC, check what is the final amount showing at checkout after cashback for the below product

www.amazon.in/Acer-Splendor-Monitor-Technology-Eyesafe/dp/B0B5PQYLSQ

Yes you should on 20,495. Would arrive as Amazon Pay Balance.@solo_wing would you still get 5% Cashback on top of the Instant Bank Discount?

Amozon pay card gives 5% INSTANT an d 5% Cashback.Can anyone with Amazon Pay ICICI Bank CC, check what is the final amount showing at checkout after cashback for the below product

www.amazon.in/Acer-Splendor-Monitor-Technology-Eyesafe/dp/B0B5PQYLSQ

So there's a slight benefit if one goes for the EMI option?Amozon pay card gives 5% INSTANT an d 5% Cashback.

NON amazon ICICI , 10% instant capped at 1500 for Full Swipe and 2000 for EMI ( it will incurr additional 199+ GST@18% + 18%GST on interest)

Kotak card has 10% capped at 1500

Amozon pay card gives 5% INSTANT an d 5% Cashback.

NON amazon ICICI , 10% instant capped at 1500 for Full Swipe and 2000 for EMI ( it will incurr additional 199+ GST@18% + 18%GST on interest)

Kotak card has 10% capped at 1500

NOTE:-

Sometimes, i like to place order USING NO COST EMI options to spread out spending on my CC.

This doesnot in anyway affect your order or cost.You will get the benefit of INSTANT DISCOUNT.

I even forward any additional discount left after deducting all associated costs like EMI Fees etc. on EMI payment option.

It is at my discretion how i choose to make the payment i.e. FULL SWIPE or NO COST EMI.

Large transactions on CC are monitored by IT dapartment and will lead to unnecessary notice.So there's a slight benefit if one goes for the EMI option?

What does spread out spending on CC mean?

Interesting. Thanks for the tip.Large transactions on CC are monitored by IT dapartment and will lead to unnecessary notice.

So i prefer to keep monthly payments under 1lac per card.

EMIs also improves Credit rating, another benefit of chosing EMI payments.

Yes, sometimes there is additional discount on EMI.So there's a slight benefit if one goes for the EMI option?

Absolute limit is 10 lakh spend in a financial year under a PAN on credit cards from any bank but there have been cases in the past where spend slightly below 10 lakh in a financial year was also reported by banks to IT department.Large transactions on CC are monitored by IT dapartment and will lead to unnecessary notice.

So i prefer to keep monthly payments under 1lac per card.

EMIs also improves Credit rating, another benefit of chosing EMI payments.

I don't spend that much but it's good to knowAbsolute limit is 10 lakh spend in a financial year under a PAN on credit cards from any bank but there have been cases in the past where spend slightly below 10 lakh in a financial year was also reported by banks to IT department.

@kingabraham

Type of purchase and other factors also determine if they will serve you notice.Absolute limit is 10 lakh spend in a financial year under a PAN on credit cards from any bank but there have been cases in the past where spend slightly below 10 lakh in a financial year was also reported by banks to IT department.

@kingabraham

Yes but most important factor is still the mismatch between the ITR you file & the amount you spend on your cards. Somebody filing 5 lakh ITR but spending 10 lakh on credit cards will likely get a notice sooner or later(may even take 2-3 years).Type of purchase and other factors also determine if they will serve you notice.

Suppose if you purchase GOLD or jewelery or making foreign payments, there are high chances that they will serve you notice.

I can help.Does anyone have SBI credit card? Need help purchasing a 30k laptop from flipkart